The U.S. energy sector has enjoyed bumper profits in the current year, with Big Oil companies setting records left, right and center. And Wall Street is saying the party is set to continue in the coming year. According to a recent Moody’s research report, U.S. industry earnings will stabilize overall in 2023, but remain relatively high. The analysts note that commodity prices have declined from very high levels earlier in 2022, but have predicted that prices are likely to remain cyclically strong through 2023. This, combined with modest growth in volumes, will support strong cash flow generation for oil and gas producers. Moody’s estimates that the U.S. energy sector’s EBITDA for 2022 will clock in at $$623B but fall to $585B in 2023. The analysts say that low capex, rising uncertainty about the expansion of future supplies and high geopolitical risk premium will, however, continue to support cyclically high oil prices. Meanwhile, strong export demand for U.S. LNG will continue supporting high natural gas prices.

With some of the strongest earnings in the market, U.S. energy companies are likely to remain good buys in the coming year. But some experts are now saying their neighbors to the north also deserve a second look.

After a umper year of share buybacks and dividends, BMO Capital Markets analysts have predicted that debt-light Canadian oil and gas producers are poised to reward shareholders even more in 2023 thanks to their ability to generate ample cash coupled with their diminished appetite for acquisitions.

BMO estimates that the top 35 energy companies will generate C$54 billion ($39.7 billion) in free cash flow in 2023, 16% lower than this year. However, the analysts say that the portion of cash that flows to shareholders is likely to be higher because companies will spend less on debt repayment.

According to the analysts, most large- and mid-size producers expect to be net-debt-free in the second half of 2023. Net debt represents a company’s gross debt minus cash and cash-like assets

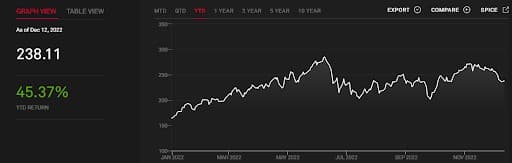

The TSX Energy Index is up 45.4% in the year-to-date, not far from the 49.8% return by its United States brethren, the S&P 500 Energy Index.

S&P/TSX ENERGY

Source: S&P

Canadian Energy Stocks

BMO notes that Canadian energy stocks have lately come under heavier pressure than their U.S. counterparts during the latest oil price selloff due to a number of factors including discount for their heavy-grade crude and also a $29 per barrel discount due to distance from U.S. refineries. The analysts have warned that the discount may worsen following the shutdown of the Keystone Pipeline.

BMO has tapped Bonterra Energy Corp. (OTCPK: BNEFF) and Canadian Natural Resources (NYSE: CNQ) as good buys.

Bonterra Energy Corp., a conventional oil and gas company, engages in the development and production of oil and natural gas in the Western Canadian Sedimentary Basin. Its principal properties include Pembina and Willesden Green Cardium fields located in central Alberta. The company faced a severe crisis in 2020 when the COVID-19 pandemic crushed oil prices. Luckily, a government-backed loan helpedBonterra through the dark times. Bonterra has managed to repay the loan, along with C$150 million in debt during the past year as of the third quarter. According to Chief Executive Officer Pat Oliver, the company expects to pay off its remaining C$38 million bank debt by the third quarter 2023, after which it will have new options like initiating a dividend, raising production or repaying debt further.

Meanwhile, Canada’s biggest oil producer Canadian Natural Resources announced last month that it will raise shareholder returns to 80% to 100% of free cash flow up from 50%, once it brings down net debt to C$8 billion. BMO says this is likely to happen late next year.

We recommend Arc Resources (OTCPK: AETUF), Enbridge Inc. (NYSE: ENB) and Cenovus Energy (NYSE: CVE).

ARC Resources Ltd. explores, develops, and produces crude oil, natural gas, and natural gas liquids in Canada. We like the company due to its very conservative debt level and better credit rating than most of its peers. Further, its February merger with Seven Generations Energy Ltd. for $2.7-billion in stock that made the combined entity Canada’s largest condensate producer and third-largest natural gas producer has proven to be profitable. Last month, Arc Resources declared a CAD 0.15/share quarterly dividend, good for 25% increase from prior dividend of CAD 0.12. The shares now yield 3.34%.

Enbridge Inc. operates as an energy infrastructure company. The company operates through five segments: Liquids Pipelines, Gas Transmission and Midstream, Gas Distribution and Storage, Renewable Power Generation, and Energy Services. Last month, Enbridge told shareholders that it expects to generate strong business growth in 2023, forecasting full-year EBITDA of C$15.9B-C$16.5B. Enbridge attributes the gain to contribution from $3.8B of assets to be placed into service this year, as well as strong expected utilization of assets across core businesses.

Cenovus Energy Inc. develops, produces, and markets crude oil, natural gas liquids, and natural gas in Canada, the United States, and the Asia Pacific region. Cenovus Energy currently returns 50% of excess free cash flow to shareholders, and has said it will increase that to 100% of excess free cash flow when the net debt level drops to C$4 billion of net debt.

Last week, Cenovus guided for production of 800K-840K boe/day next year, an increase of more than 3% Y/Y, including oil sands production of 582K-642K boe/day and conventional output of 125K-140K boe/day. The company said that total downstream crude throughput is forecast at 610K-660K bbl/day, up nearly 28% Y/Y.

SOURCE:https://oilprice.com/