Chart of the Week

– The 50-day implied volatility rate of oil jumped some 16% amidst the ongoing chaos surrounding the collapse of SVB and Signature Bank, the most since the beginning of the Russia-Ukraine war.

– With U.S. headline CPI coming in at 6% in February, the balancing act of the Federal Reserve might render the oil markets more volatile again as higher inflation for longer undermines demand growth but also cuts into supply prospects.

– In just one day of trading on April 13, the open interest held in ICE Brent contracts decreased by almost 35,000 lots (equivalent to 35 million barrels) whilst the response in WTI NYMEX was much more subdued.

– As both WTI and Brent shed almost $5 per barrel week-on-week, it is the Middle Eastern benchmark Dubai that has come out of the chaos relatively unscathed, being already on par with Brent and showing the resilience of Asian markets.

Market Movers

– Chinese oil major Sinopec (SHA:600028) has proposed to fully finance the construction of the planned 100,000 b/d Hambantota refinery in Sri Lanka, in a blow to Indian interests there.

– Brazilian oil major Petrobras (NYSE:PBR) has chartered two drilling rigs for a two-well 2024 drilling campaign that could confirm the deepwater prospects of Colombia’s offshore zone after a pioneering discovery there in July 2022.

– U.S. refiner Marathon Petroleum (NYSE:MPC) will take 8.4 million barrels from the upcoming 26 MMbbls SPR release, followed by Norway’s Equinor (NYSE:EQNR) and the UK’s Shell (LON:SHEL).

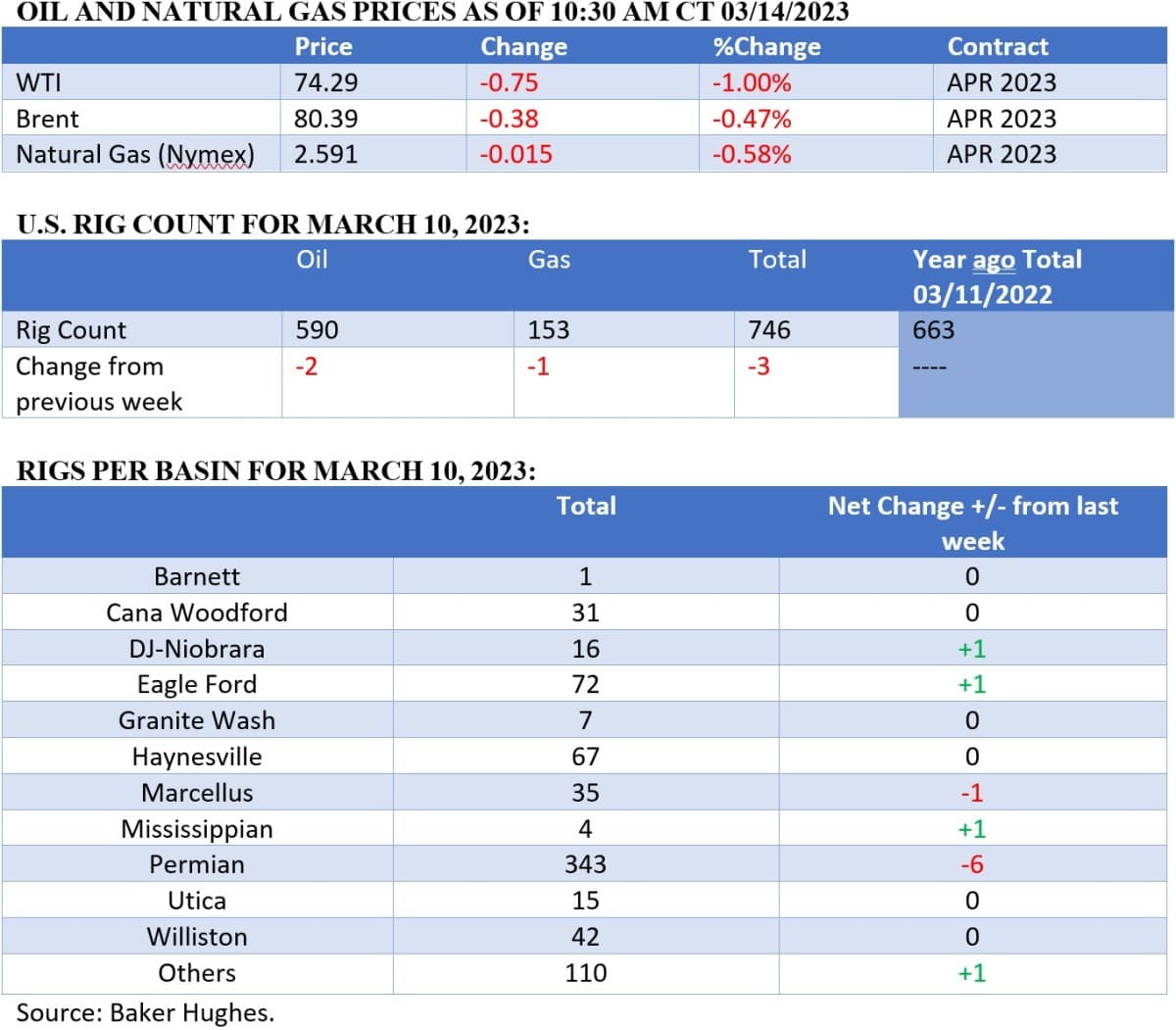

Tuesday, March 14, 2023

The collapse of Silicon Valley Bank and the risks of seeing other U.S. banks going down the drain have shaken the oil markets, sending WTI below $75 per barrel and Brent below the $80 per barrel mark. The oil narrative has been almost completely taken over by macro news, as even the relatively few newsworthy stories to come out did not provide any surprises – OPEC oil demand growth is still 2.3 million b/d and U.S. oil inventories seem to be relatively stagnant.

OPEC Upbeat on Chinese Demand. In its latest Monthly Oil Market Report, OPEC increased its 2023 oil demand growth forecast for China to a 0.71 million b/d year-on-year hike thanks to strong diesel and jet fuel increases, with the Asian powerhouse accounting for a third of global growth this year.

Iran Exports Reach Sanctions-Era Peak. Iran’s oil minister Javad Owji stated the Middle Eastern country’s oil exports have reached the highest level since Donald Trump reimposed US sanctions in late 2018, averaging above 1 million b/d every month since November 2022.

Saudi Aramco Hikes 2023 Capex Amidst Record Profits. Raking in $161.1 billion in 2022 net income, the Saudi national oil company Saudi Aramco (TADAWUL:2222) will boost capital expenditures to up to $55 billion, focusing on new production capacity in offshore oil and gas fields. Related: LNG Market Could Become Too Saturated By 2027

EU Wants to Weaken Car Emission Rules. A group of EU members led by Germany and Italy are pushing for the relaxation of Euro 7 mandates that tighten limits on vehicle pollutants such as nitrogen oxides, which Brussels wants to see enacted by mid-2025 giving carmakers little time to adapt.

Plaquemines Phase 2 Gets The FID. Less than 10 months after sanctioning phase one of the Plaquemines LNG project in Louisiana, the final investment decision for the 2nd phase totaling 10.7 mtpa of liquefaction capacity has been greenlighted this week after securing $7.8 billion in financing.

French Strikes Disrupt LNG Send-outs. France has been paralyzed by ongoing protests against President Macron’s decision to raise the retirement age by 2 years to 64, with all four of its LNG import terminals blocked since last week, pushing front-month TTF prices back to €50 per MWh.

India Warns Against Using Yuan. As India is buying increasing amounts of Russian oil and coal, the country’s authorities have asked banks and traders to avoid using Chinese yuan for energy imports and use the UAE dirham instead, due to long-standing political differences with its neighbor.

Ford-CATL Deal Under Congress Scrutiny. U.S. Senator Joe Manchin (D-WV) lambasted the deal between Chinese battery maker CATL (SHE:300750) and carmaker Ford (NYSE:F), saying that the 12% royalty rate would send $900 of the $7,500 EV tax credit that the IRA bill stipulates to China.

White House Greenlights Alaskan Oil Project. The Biden Administration approved a scaled-back version of ConocoPhilips’ $7 billion Willow oil and gas project in the northern part of Alaska that is estimated to hold 600 MMbbls, immediately triggering the ire of environmentalists.

UK Pension Funds Go After Oil Majors. Two of Great Britain’s largest pension funds threatened to vote against the renewal of top officials at BP (NYSE:BP) and Shell (LON:SHEL) unless both oil majors render their carbon emissions-cutting commitments more stringent.

The Year of the Solar Rebound. U.S. restrictions on Chinese solar panels produced in the Xinjiang region decreased solar installations across the country by 16%, however, the markets are expecting a robust rebound in 2023 with 41% year-on-year growth aided by the Inflation Reduction Act.

Russia Agrees to Extension of Black Sea Grain Deal. Russian authorities claimed they’ve agreed to a 60-day extension of the Black Sea grain deal, expiring on March 18, out of “goodwill” and pressed the UN for the full resumption of fertilizer and ammonia exports.

SVB Collapse Threatens U.S. Renewable Plans. The now-failed Silicon Valley Bank has been a major lender to community solar projects and its collapse could jeopardize the buildout of smaller than utility-scale solar farms, currently at a capacity of 5.6 GW.

Source: https://oilprice.com/